Mortgage Rates Forecast For 2024: Experts Predict How Much Rates Will Drop – Forbes

Mortgage rates just can’t seem to get into a sustainable downward groove.

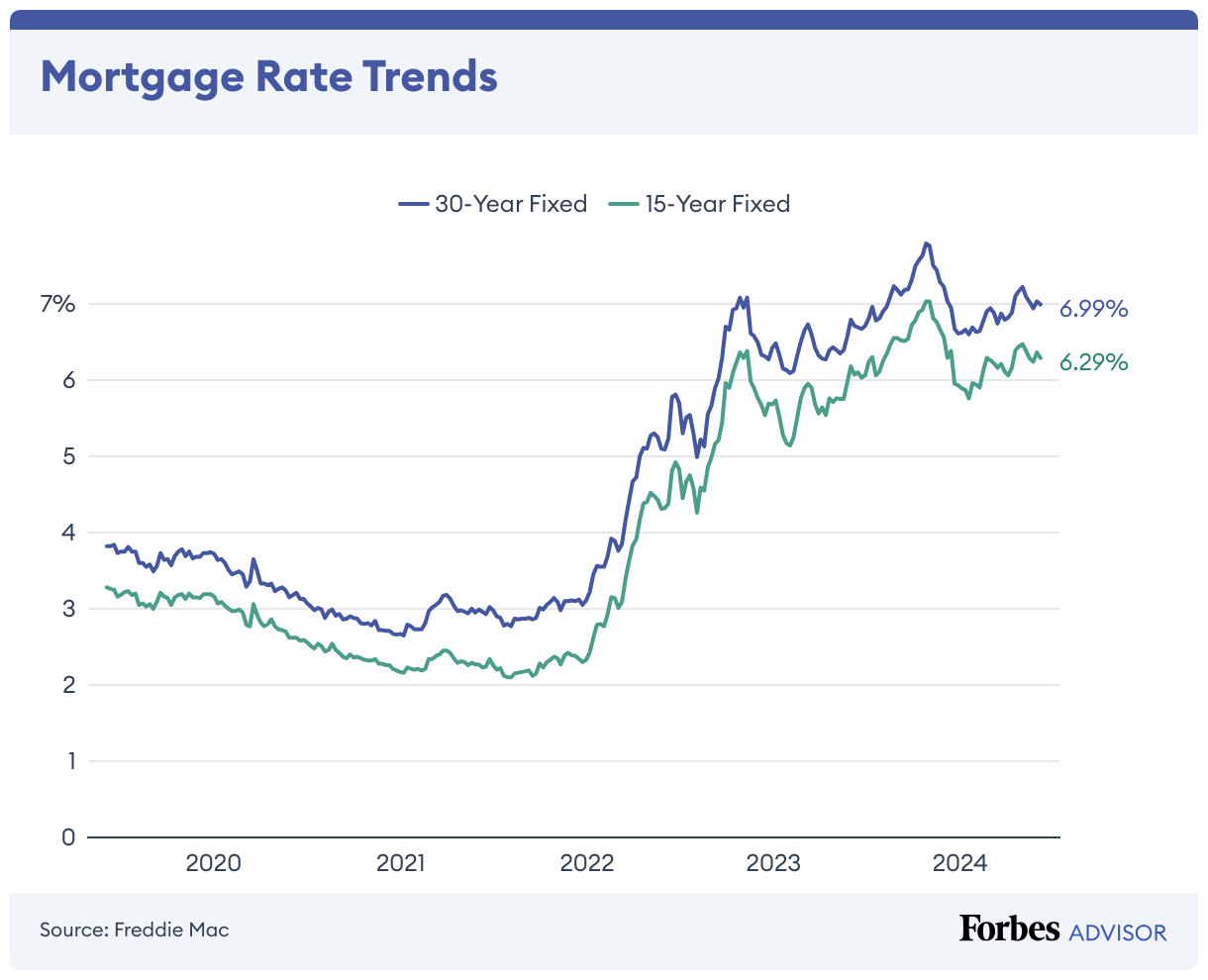

After hitting a 2024 high of 7.22% to start May, the average 30-year fixed mortgage rate dropped 19 basis points over the course of the month before rising above 7% again at the end of the month. A basis point is one one-hundredth of a percentage point.

Buy/sell, rent/lease residential &

commercials real estate properties.

For the week ending June 6, the 30-year fixed rate sat at 6.99%, according to Freddie Mac.

Many housing market experts don’t expect mortgage rates to recede significantly in the coming months unless the Federal Reserve decides to cut its benchmark interest rate.

Mortgage Rate Predictions for 2024

Here is how some experts predict market conditions will affect the average 30-year, fixed-rate mortgage in 2024:

Freddie Mac: Rates will remain above 6.5% through Q2

Freddie Mac maintains that mortgage rates will stay above 6.5% through the first half of 2024, per its March Economic, Housing and Mortgage Market Outlook forecast. In its May forecast, the mortgage giant anticipates the central bank will cut the federal funds rate only once this year, keeping mortgage rates elevated for the remainder of 2024.

Fannie Mae: Rates will average 7.1% in Q3

Fannie Mae revised its anticipated average 30-year fixed mortgage rate trajectory. In its April housing forecast, Fannie Mae projected rates to average 6.6% in Q3 but has since revised this to 7.1%. Moreover, the May forecast predicts that mortgage rates will average 7% in 2024, up from 6.6%.

“For now, we see rates remaining closer to 7 percent through the end of the year—before trending downward in 2025—but note potential downside to that forecast given recent actual movements in rates,” said senior vice president and chief economist Doug Duncan, in a recent press release.

National Association of Realtors (NAR): Rates will average 6.7% in Q3

NAR expects the 30-year fixed mortgage rate to average 6.7% in its most recent quarterly forecast published in April but decline to 6.5% by the end of 2024, assuming the Fed cuts rates.

“The Federal Reserve is delaying and is cautious about inflation, but 6 to 8 rounds of rate cuts through the end of 2025 are likely to bring the interest rates down from current high levels to match those during the pre-COVID years,” said chief economist Lawrence Yun, in a May press statement. “Do not expect any major declines in mortgage rates, however.”

Mortgage Bankers Association (MBA): Rates will decline to 6.7% in Q3

MBA expects the 30-year fixed-rate mortgage to decline throughout the year, averaging 6.7% in Q3, according to its May Mortgage Finance Forecast. MBA economists expect the Fed to implement a rate cut in September and one more before the end of the year, with the average mortgage rate landing around 6.5% by the end of 2024.

Bank of America: Rates will decline below 7%

“Bank of America global economists now anticipate the first rate cut in December,” says head of retail lending Matt Vernon. “While there’s still optimism that mortgage rates will eventually drop below 7% in the coming months, inflationary pressures are currently keeping them elevated.”

KPMG Economics: Rates will likely stay within the 7% range through Q2

“We could still see one [Fed] rate cut at the end of the year, but any reacceleration in inflation will push cuts even further,” says senior economist Yelena Maleyev. “The bulk of the declines in rates will occur in 2025; mortgage rates could remain close to 7% for the busy spring home-buying season.”

Palisades Group: Rates will stay above 6.25% through 2024

“The market has consistently overestimated the likelihood, timing, and quantity of the Federal Reserve’s rate cuts,” says managing member and chief investment officer Jack Macdowell. “Based on current data, it is hard to envision more than one to two cuts in 2024 and hard to see mortgage rates drop below 6.25%.”

Advisor Credit Exchange: Rates will range between 7% and 7.5% in the coming months

“Until the Federal Reserve can prove to the markets that inflation is under (and remains under) control, inflation will continue to have a magnified impact on the 10-year Treasury and ultimately mortgage rates,” says Bob Smith, head of real estate. “I expect mortgage rates to remain in a bounded range until this gets sorted out and expect minimal impact from any Fed decisions in June.”

Fed Holds Rates Steady, Again: What This Means for Mortgage Rates in 2024

In an unsurprising move, the Federal Open Market Committee (FOMC) announced on May 1 after its latest two-day policy meeting that officials voted unanimously to leave the benchmark federal funds rate unchanged. The federal funds rate is the overnight borrowing rate for commercial banks and credit unions and indirectly influences mortgage rates.

The decision marks the sixth consecutive meeting in which the FOMC has kept its policy rate steady between 5.25% and 5.5%.

Over the past two years, mortgage rates have skyrocketed to their highest levels in decades amid the Fed’s efforts to tame inflation through aggressive interest rate policy actions.

Though many housing industry experts predicted mortgage rates would begin to recede in 2024 as the Fed implemented rate cuts, mortgage rates have surged. This is due partly to signals that the Fed will need to hold rates “higher for longer” as a result of hotter-than-expected inflation readings and a strong labor market.

Due to the stalled progress of lowering inflation to the Fed’s 2% goal, some policymakers have recently stated that there is no urgency to cut rates this year, with one Fed official hinting that a rate hike may be warranted. However, Powell noted at the press conference following the rate announcement that it’s “unlikely that the next policy rate move will be a hike.”

So, what does all this mean for mortgage rates?

“In order to see mortgage rates drop more significantly, the Fed will need to see more evidence that inflation is slowing,” said Danielle Hale, chief economist at Realtor.com, in an emailed statement. “My expectation is that it will take longer, and that sets the Fed up for a late summer or early fall adjustment, and mortgage rates could follow suit.”

Melissa Cohn, regional vice president of William Raveis Mortgage is less optimistic about the timing of rate cuts.

“Based on where the economy has gone, we may not see anything until 2025,” said Cohn in an emailed statement.

Consequently, Cohn advises against waiting to jump into the market if you’re keen on buying a home.

“If you buy now before interest rates really come down and prices go up, you are still ahead of the game, even if you’re paying more in a mortgage payment for a short period of time,” Cohn said.

Despite elevated mortgage rates, Hale says buyers can secure a lower rate by comparing lenders or shopping for homes with an assumable mortgage, which is when a seller allows a buyer to take over an existing mortgage and (typically lower) rate. Hale says this hack “can result in lower costs and make home buying possible even before mortgage rates trend more meaningfully lower.”

The next two-day FOMC meeting is June 11 and 12. Policy makers are expected to hold the federal funds rate steady, according to the CME FedWatch Tool, an online barometer that gauges market expectations for rate cuts or hikes at upcoming FOMC meetings.

Is 2024 a Good Time To Refinance?

Whether or not 2024 will be a good time to refinance depends on several factors, including if the Fed cuts interest rates this year and by how much. The mortgage rate you got when you financed your home is another major factor.

Over 40% of U.S. mortgages originated in 2020 and 2021, when interest rates were at record lows. There were also some 14 million mortgage refinances during the same time. If you were lucky enough to secure a mortgage during that time, then 2024 is likely not the ideal time to refinance.

– Glenn Brunker, president of Ally Home

“If rates are lower than when you first got your mortgage, it might be a favorable time,” says Vernon. However, whether rates go lower in 2024 will depend, in part, on economic conditions.

Experts believe that once the Fed cuts rates in 2024, refinance volume will improve as borrowers who took on high mortgage rates will jump at the chance to lower their monthly costs.

“If [mortgage] interest rates dropped to even 5.5%, it could result in significant savings for these homeowners, as refinancing at that rate could result in an average monthly payment of $1,917 for them, a reduction of $284 every month,” said Michele Raneri, vice president of U.S. research and consulting at TransUnion, in an emailed statement.

If you’re considering refinancing to lower your monthly payment, keep in mind that not all options yield less interest over the life of the loan.

However, the prospect of a rate cut in the next few months has begun to fade amid persistent inflation and resilient economic data.

Nonetheless, if you’re considering refinancing to lower your monthly payment, keep in mind that not all options yield less interest over the life of the loan.

“Remember that just because you can get a lower rate doesn’t mean you should immediately refinance,” says Vernon. “You may be paying a lower monthly mortgage, but you may have to also extend the life of your loan and refinancing could cost you more in interest.”

Current Mortgage Rate Trends

What Do Current Rates Mean for Refinancing in 2024?

Refinance volume remains at low levels. Here’s how refinance activity has trended recently, according to the MBA’s Weekly Mortgage Applications Survey.

| Refinance Activity | Weekly | Annually |

|---|---|---|

|

Week ending May 8

|

+5%

|

-6%

|

|

Week ending May 15

|

+5%

|

+7%

|

|

Week ending May 22

|

+7%

|

+21%

|

|

Week ending May 29

|

-14%

|

+12%

|

For those who hoped to refinance in 2024 when mortgage rates were supposed to recede enough to make refinancing worthwhile, stubborn inflation and the Fed maintaining its benchmark interest rate at a two-decade high have doused those hopes.

By the end of May, the average 30-year fixed mortgage rate of 7.03% was nearly a quarter of a percentage point higher than the same week a year ago—and refinance rates tend to be higher than purchase rates.

Meanwhile, many borrowers are sitting on the historically low mortgage rates they nabbed during the pandemic. Currently, over six out of 10 purchase and refinance loans are at rates below 4%, according to Freddie Mac. Those ultra-low rates are unlikely to return anytime soon—if at all—resulting in limited motivation for many homeowners to refinance.

At the same time, mortgage rate volatility continues to be a defining feature of 2024, leading to ups and downs in refinance activity.

“Borrowers remain sensitive to small increases in rates, impacting the refinance market and keeping purchase applications below last year’s levels,” said Joel Kan, vice president and deputy chief economist at MBA, in a press statement.

How To Get a Lower Mortgage Refinance Rate

The good news is that, despite elevated rates, there are methods you can employ to secure a lower rate. These methods might be especially beneficial if you bought a home between mid-October and early November 2022 or mid-August through early December 2023 when rates were over 7%.

Because there are closing costs and fees associated with refinancing, many mortgage experts say refinancing only makes sense if you can snag a rate that’s at least 1% lower than your current rate.

Here are some actions you can take to whittle down your refinance rate:

- Get rate quote estimates from at least three lenders

- Ask lenders about waiving or reducing closing costs

- Negotiate with your lender to match the best deal

- Take steps to strengthen your credit score

- Save for a larger down payment

- Choose a shorter-term loan

- Buy discount points

Mortgage Rate Predictions for the Next 5 Years

While predicting mortgage rates for the next five years is a tall order, especially considering the unprecedented fluctuations over the past year, experts say the low housing inventory will be a key factor in where rates go over the long term.

“When rates come down, we’re going to be in store for another hot housing market where there are more buyers than sellers jacking up prices because we haven’t solved the problem” of low inventory, says Daryl Fairweather, chief economist at Redfin. “It’s still that affordability problem. That’s going to stay with us.”

As far as which direction interest rates go in the years ahead, Fairweather expects declines. However, the timeline for this downward trend remains uncertain.

“In every scenario, rates are going to come back down,” says Melissa Cohn, regional vice president at William Raveis Mortgage. “It’s just a matter of when.”

That “when” for Cohn won’t be in the immediate future—but she doesn’t see it as too far off.

“Mortgage rates will decline over the course of the next two to three years as the rate of inflation declines and hopefully gets to the Fed target of 2%,” Cohn says. “Mortgage rates will be at least a full 2% lower by 2025.”

She adds that if the inflation rate holds at 2%, then we should see mortgage rates remain at lower levels for the balance of the next five years.

What Affects Mortgage Rates?

A complex set of factors impact mortgage interest rates, including broader economic conditions, the monetary actions of the Federal Reserve (to some extent) and inflation. However, long-term mortgage rates are directly impacted by the bond market. The rate you’re offered on a mortgage will also depend on the lender you work with, its business costs and your financial profile.

Demand for mortgages can also affect rates, pushing them higher as available capital for lending tightens. Conversely, when there’s less borrower demand—as we’re seeing now due to average interest rates hovering in the high 6% to low 7% range—lenders might consider offering more competitive rates or other incentives to attract borrowers.

How To Shop For the Best Mortgage Rate

– Matt Vernon, head of retail lending, Bank of America

Getting an optimal rate on a home loan can save you a significant amount of money over time. Here are some tips that can help you get the best rate possible for your situation:

- Keep your eye on rates. Mortgage rates are constantly changing. Keeping a close watch will make it easier to find and lock in a better rate.

- Check your credit. When you apply for a mortgage, the lender will review your credit to determine your creditworthiness as well as your interest rate. In general, the higher your credit score, the better your rate will be. To get an idea of where you stand, check your credit before you apply and dispute any errors with the appropriate credit bureau to potentially boost your score.

- Shop around and compare lenders. Consider options from as many mortgage lenders as possible to find the best deal for you. Prospective buyers have saved more than $1,500 over a loan’s term by getting two quotes from lenders and saved roughly $3,000 when they sought five quotes, according to Freddie Mac.

Faster, easier mortgage lending

Check your rates today with Better Mortgage.

Frequently Asked Questions (FAQs)

What are mortgage rates?

Mortgage rates are the costs associated with taking out a loan to finance a home purchase. Because properties cost so much, most people can’t pay for them with cash, so they opt to stretch the payments over long periods of time, often as much as 30 years, to make the regular monthly payments more affordable.

When interest rates rise, reflecting changes in the economy and financial markets, so too do mortgage rates—and vice versa.

What is a mortgage rate lock?

A mortgage rate lock is a guarantee that the rate you’re offered in your mortgage application acceptance is the one you will eventually pay, assuming you close within a normal period of time and make no changes to your application.

In a period of rising or volatile interest rates—like the present one—it may be wise to lock in a rate that seems affordable for you.

When should I lock my mortgage rate?

It can be tricky to time any market, and mortgage rates are no exception. If conditions are choppy, and interest rates are likely to rise, it may be smart to lock in a rate that works with your budget and seems fair to you.

Be sure to ask your lender about the consequences of not closing within the timeframe specified in a rate lock agreement and also about what could happen if rates fall after you lock in a rate.

How do you calculate your mortgage payment?

Depending on your loan type and other factors, the components of a monthly payment can vary but typically include:

- Principal. The amount of funds you borrow from a lender for your mortgage.

- Interest. The cost the lender charges you for borrowing the funds.

- Property taxes. Payments are based on local property tax rates.

- Homeowners insurance. A separate policy for insurance coverage based on the value of your home and property.

- Private mortgage insurance (PMI). Typically only applies if you take out a conventional mortgage with a down payment below 20% of the purchase price.

- Homeowners association (HOA) or condominium fees. Only applies if your property is part of an HOA or you own a condominium.

- Escrow. An account reserved for property taxes, homeowners insurance and mortgage insurance, managed by the lender.

- Additional costs. Examples of potential additional costs include home warranties and flood insurance.

Along with the above information, plug in the home price, down payment, interest rate and loan term into a mortgage calculator to determine the most accurate monthly mortgage payment estimate.

Will mortgage rates go down in 2024?

Given the many factors that directly and indirectly impact mortgage rates, predicting where rates will go in the years ahead is tricky. Nonetheless, experts foresee an inevitable downward trend, though probably not in the immediate future.

“[O]ur economic models don’t show mortgage interest rates declining anytime soon,” says Eric Fox, chief economist and senior vice president of analytics for Veros Real Estate Solutions. “Long term into 2024, we will see interest rates starting to have the desired impact in slowing the economy, but rates will need to remain elevated for some time.”

Fox says his models suggest that rates will hover at 7.5% or higher throughout 2024.

What is the mortgage rate forecast for the next five years?

The Fed’s economic projections indicate the federal funds rate will remain higher through 2025 and in the longer run than previously expected. Nevertheless, the projections show that cuts are in store. If those projections remain and the Fed begins to lower its key rate, mortgage rates will presumably follow suit.

Sunbury predicts the Fed will cut rates by between 100 to 125 basis points starting in May or June of 2024.

“This would bring the policy rate to 4% to 4.25%,” Sunbury explains.

And though Sunbury forecasts mortgage rates dropping, she doesn’t anticipate the imminent return of the rock-bottom rates we saw in 2021 and 2022.

“As inflation eases and the policy rate comes down, we should see 30-year fixed mortgage rates come down to the 5.5% to 6% range and remain around this range longer term,” she says.