Losses Pile Up in Top-Rated Bonds Backed by Commercial Real Estate Debt – Yahoo Finance

(Bloomberg) — For the first time since the financial crisis, investors in top-rated bonds backed by commercial real estate debt are getting hit with losses.

Most Read from Bloomberg

Buy/sell, rent/lease residential &

commercials real estate properties.

Buyers of the AAA portion of a $308 million note backed by the mortgage on the 1740 Broadway building in midtown Manhattan got less than three-quarters of their original investment back earlier this month after the loan was sold at a steep discount. It’s the first such loss of the post-crisis era, according to Barclays Plc. All five groups of lower ranking creditors were wiped out.

Market watchers say the fact the pain is reaching all the way up to top-ranked holders, overwhelming safeguards put in place to ensure their full repayment, is a testament to how deeply distressed pockets of the US commercial real estate market have become.

Bonds backed by single mortgages and tied to older office buildings dominated by one anchor tenant — like 1740 Broadway — are especially vulnerable, they say. Some analysts are already predicting further losses as more loans get sold for a fraction of their former value.

“Now that we’ve seen the first commercial mortgage backed securities get hit, other AAA bonds are bound to see losses,” said Lea Overby, a CMBS strategist at Barclays. “These losses may be a sign that the commercial real estate market is starting to hit rock bottom.”

With about $700 billion of non-agency CMBS outstanding and another $3 trillion of commercial mortgages on bank balance sheets, even a modest uptick in losses could weigh on the financial system for years.

To be clear, no one is predicting a repeat of 2008, when bad mortgages, mostly residential, nearly brought down the financial system.

Yet the risk isn’t simply confined to a handful of underperforming buildings, either.

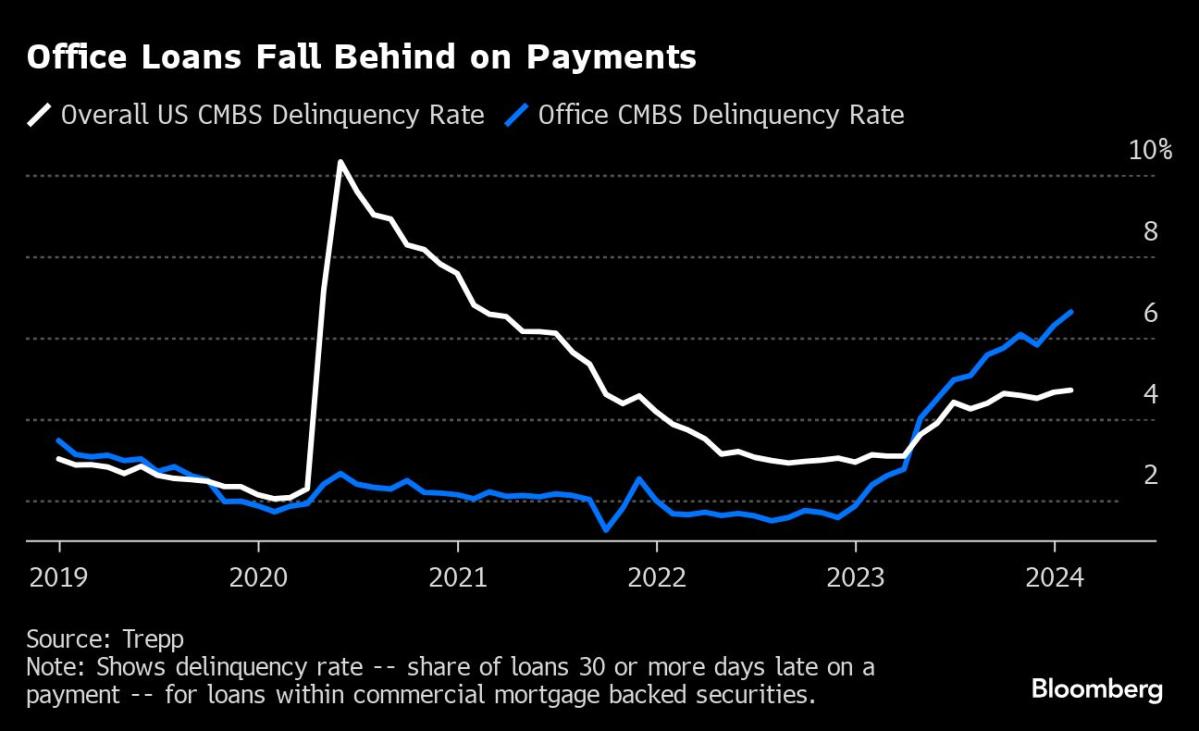

The share of delinquent office loans packaged into a common type of commercial mortgage backed security reached 6.4% in April, the highest since June 2018, according to a report by Moody’s Ratings this month.

More than that, about $52 billion, or 31%, of all office loans in commercial mortgage bonds were in trouble in March, according to KBRA Analytics, up from 16% a year ago. The assessment includes both single-asset single-borrower and so-called conduit CMBS wherein mortgages are pooled together. Some cities are facing more stress than others, with 75% of CMBS office loans in Chicago and 65% in Denver in jeopardy, according to the firm.

“Values have plunged because of the combination of rising interest rates, which means increasing investment, as well as decreasing cash flow,” said Harold Bordwin, a principal at Keen-Summit Capital Partners, which specializes in renegotiating distressed real estate. “The consequence is equity will have significant losses and secured debt holders, their investment is impaired.

The 1740 Broadway building, formerly the Mutual of New York or MONY building, sits just south of Columbus Circle between 55th and 56th streets. Built in 1950, the letters formerly atop the building inspired the title to the hit 1968 song “Mony Mony” by Tommy James and the Shondells.

It was bought for $605 million by Blackstone Inc. in 2014. To help finance the deal the firm took out a $308 million mortgage, which was packaged into a CMBS and scooped up by the likes of Travelers Cos., Endurance American Insurance Co. and others.

In 2021 L Brands, the former parent of Victoria’s Secret and Bath & Body Works that occupied 77% of the property’s leased space, said it would exit the tower. While Blackstone spent tens of millions of dollars to modernize the building, tepid demand for office space made finding new tenants difficult. With no one paying rent, Blackstone stepped away from the property in 2022, defaulting on the loan.

A few weeks ago, the mortgage’s special servicer and Blackstone agreed to sell the building to Yellowstone Real Estate for roughly $186 million, according to people familiar with the matter. The deal resulted in the repayment of the CMBS. But with additional losses from fees and advances, only $117 million was left for bondholders. Investors in $151 million of lower-rated debt were wiped out, while those holding $158 million of debt originally rated AAA suffered a 26% loss.

“This deal was a perfect storm of an office building that relies on one tenant for the majority of the rent,” John Kerschner, head of US securitized products at Janus Henderson, said in an interview. “We will see more bonds get hit related to the office space, but it’s going to take some time. Leases and office mortgages are very long-dated.”

In an emailed response to questions a Blackstone spokesperson said the firm “wrote this property off nearly three years ago. Less than 2% of our owned portfolio is traditional U.S. office. This is not a new development and is a rare instance in our nearly $600 billion portfolio.”

A representative for Yellowstone didn’t respond to a request seeking comment.

Some industry observers say CMBS investors should expect more losses on bonds originally rated AAA in the months to come.

Barclays strategists warned in a recent report that top-ranked holders of at least four commercial mortgage backed securities tied to malls, including the former Westfield San Francisco and the Palisades Center mall north of New York, are likely to get hit. Office CMBS is increasingly on their radar, they wrote.

“Because we are only in the early stages of office price discovery, we expect this list to expand to include several office deals,” Barclays’ Overby and Anuj Jain said in the report.

They flagged in particular developments at 600 California St. in San Francisco, owned in part by an affiliate of WeWork, and River North Point in Chicago, owned by Blackstone. There’s about $60 billion of office CMBS backed by single mortgages, according to Barclays estimates.

“Given the challenges facing the property, we effectively wrote it off in 2022,” a Blackstone spokesperson said via email. A representative for WeWork declined to comment.

Read More: Massive Office Tower Losses Reveal Hidden Risks Across the Globe

In north suburban Chicago, an office loan held by private equity giant Ares recently sold at just 12% of its original price. That debt was packed into a vehicle called a commercial real estate collateralized loan obligation, which are themselves facing unprecedented stress.

“It’s very rare for the AAAs to get hit, which is a more idiosyncratic case with high concentration to a single office loan,” said Tracy Chen, a portfolio manager at Brandywine Global Investment Management. “You have to be extremely cautious as the value of office buildings are less transparent due to lack of transactions, and so are the bonds tied to them.”

–With assistance from Scott Carpenter.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.